Most of those affected earned pensions in state or local government jobs, including teachers, firefighters, police officers, and other public-service employees. In general, federal employees would be affected only if they were hired before 1984. The WEP (but not the GPO) can also affect workers who earn pensions from nonprofits and employment in foreign countries.

Opponents believe the WEP and GPO make it hard to plan for retirement and unfairly target public servants, and a number of bills have been introduced to either eliminate or modify the provisions, including a recent bill with bipartisan support. However, action on these provisions might not be considered until Congress addresses broader Social Security reform.

Windfall Elimination Provision

The formula used to calculate Social Security retirement benefits considers the highest 35 years of earnings and gives lower-wage earners a larger percentage of their wages than higher earners. So someone who earned a pension in state government while not paying into Social Security and then worked 10 years in a job covered by Social Security taxes — the minimum required to receive retirement benefits — would appear to have very low earnings (due to 25 years of zero earnings) and would receive a higher benefit in relation to earnings. The WEP is meant to address this imbalance.

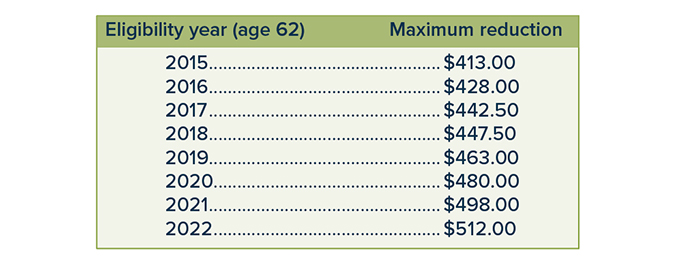

The amount of the WEP reduction depends on the year you turn 62 and the number of years with “substantial earnings” subject to Social Security payroll tax (see chart). The WEP does not apply to someone with 30 or more years of substantial earnings.2 The reduction cannot be more than one-half of the pension from noncovered employment. Because the WEP reduces the Social Security primary insurance amount (PIA), spousal and dependent benefits based on the PIA may also be reduced. The WEP does not affect survivor benefits.

WEP Reductions

Maximum monthly amount that Social Security benefits can be reduced, based on eligibility year (the year you reach age 62) and 20 years or less of substantial earnings subject to Social Security tax. The reduction amount is phased out from 21 to 30 years of substantial earnings.

If Social Security benefits start after full retirement age, or the pension from noncovered employment starts later than the eligibility year, the WEP reduction may be greater than the amounts shown. However, the reduction cannot be greater than one-half of the pension from noncovered employment.

Source: Social Security Administration, 2022

Government Pension Offset

Under the Social Security dual entitlement rule, a spouse or survivor will receive the higher of his or her own worker benefit and a spousal or survivor benefit, but cannot receive both. The GPO is intended to address the perceived unfairness of a worker receiving a pension based on noncovered employment and a spousal or survivor benefit. In this case, the GPO may reduce Social Security benefits up to two-thirds of the amount of the pension. For example, an individual who receives a $1,200 monthly pension from noncovered employment and is eligible for a $1,200 monthly Social Security spousal benefit would receive only $400 per month from Social Security ($1,200 – $800 [2/3 x $1,200] = $400). He or she would still receive the $1,200 pension, so the combined benefit would be $1,600.

For additional information, including calculators to estimate the potential reduction, see ssa.gov/benefits/retirement/planner/wep.html and ssa.gov/benefits/retirement/planner/gpo-calc.html.