If you are engaged to be married, or might be soon, it’s important to consider how this change in your relationship (and legal status) will affect your finances. Discussing the following topics well in advance may keep surprises and disagreements from disrupting your newlywed bliss.

Share debt stories. Many Americans bring college debt into their marriages, and some individuals have had bankruptcies or other severe credit challenges. Taking a close look at both credit reports may help resolve debt and credit issues before they spiral out of control.

Discuss banking and bill paying. Working together to prepare a preliminary household budget may help you start off on the right foot. If you decide not to pool all your income and assets, make sure you clearly define what belongs to each of you separately and what you will share. Some married couples use a joint account for living expenses and separate accounts for personal spending.

Look closely at company health plans. You may need to coordinate two sets of workplace benefits, so keep in mind that many companies apply a surcharge to encourage a worker’s spouse to use other available coverage. Compare the costs and benefits of having both of you on the same plan versus keeping your individual coverage with each employer.

Anticipate joint income taxes. Most married couples pay more total tax when they file separately than when they file jointly. But there are rare occasions when filing separate returns could result in a lower combined tax liability or provide another benefit. For example, if you or your fiancée have federal student loans, filing separately might help you qualify for a lower monthly payment under an income-based repayment plan. But you could also lose certain tax credits and pay more income tax, so it’s important to weigh your options carefully.

Combining your incomes could land you in a higher (or lower) tax bracket. To avoid owing money at tax time, you may want to use the estimating tool on the IRS website (irs.gov/individuals/tax-withholding-estimator) to check and adjust your employer withholding. If it turns out that you will receive a larger refund, you might reduce your withholding and put that money to better use (such as paying off debt or boosting savings).

Paying for the Party

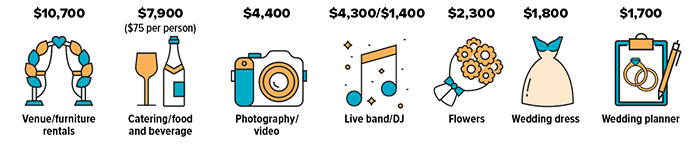

The national average cost of a wedding in 2021 was about $28,000, a figure that includes the rehearsal dinner, ceremony, and a reception with 105 guests — but not the engagement ring (which averaged $6,000) or the honeymoon. Of course, the average price tag varied greatly by location, from $16,000 in Oklahoma to $47,000 in New Jersey. With inflation soaring, many couples are facing significantly higher costs, and greater competition for in-demand vendors, in 2022.

Source: The Knot, 2022

Consider a prenuptial agreement. A prenup is a written contract that states how assets will be owned during the marriage and divided in the event of divorce. A prenup may be unnecessary if the engaged couple are both young and have comparable wealth levels. But if either partner owns (or expects to inherit) substantial assets — or has significant debts — crafting a premarital agreement may be worthwhile.

Prenups are commonly used to help protect the financial interests of children from a previous marriage or to account for other special circumstances. If a couple intends to pay off one partner’s student loans together early in the marriage, an agreement might credit the other spouse for that help in the event of a divorce. Similarly, if one partner expects to support a spouse through professional school (law or medical), an agreement may stipulate how he or she will share fairly in the professional’s future income.

You are encouraged to seek guidance from an independent tax and/or legal professional.