As the number of itemizers fell, so did the amount individuals gave to charities as a percentage of total annual contributions. According to Giving USA, the total amount dropped below 70% for the first time ever in 2018 and remained there through 2021.2

Although the primary motivation for charitable giving usually comes from a desire to give back, an associated tax break can be a strong supporting factor. If you are an IRA owner who is 70½ or older, you may be pleased to learn that you can give to charity without itemizing and still get a tax break through what’s known as a qualified charitable distribution (QCD).

How a QCD Works

Generally, distributions from traditional IRAs are subject to federal income tax, unless an exception applies. QCDs, however, are excluded from income and therefore won’t affect your tax obligation. Moreover, once you reach age 72, a QCD can satisfy all or part of your required minimum distribution (RMD), which otherwise could substantially increase your taxable income for any given year.

To make a QCD, you would direct your IRA trustee to issue a check made out to a qualified public charity. You may contribute up to $100,000 from your IRA; if you’re married, your spouse may also contribute up to $100,000 from his or her IRA.

A QCD must be an otherwise taxable distribution from an IRA. If you’ve made nondeductible IRA contributions, then each distribution normally carries with it a pro-rata amount of taxable and nontaxable dollars. If you have multiple IRAs, they are aggregated to determine the calculation. With QCDs, the pro-rata rule is ignored, and taxable dollars are treated as distributed first.

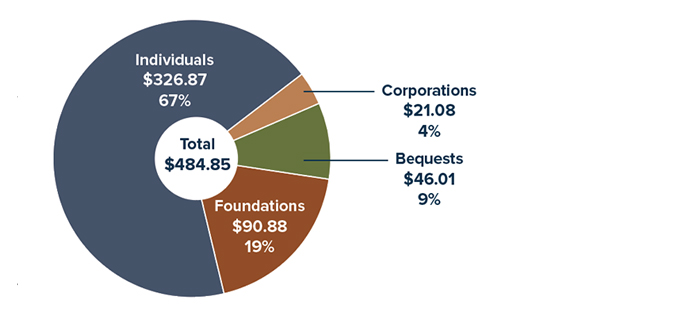

Charitable Giving by Source, 2021 (in billions)

Source: Giving USA, 2022 (total may not equal 100% due to rounding)

QCDs come with a few caveats:

- If you have a checkbook IRA, you may also write a check directly to the charity; however, the contribution will count as a QCD for the year in which it is cashed, not the year it is written. This is particularly worth noting for donations made late in the year.

- You can take a QCD from SEP and SIMPLE IRAs, but only if they’re “inactive,” i.e., have not received any contributions in the same year.

- You cannot deduct a QCD as a charitable contribution on your federal income tax return.

- As of 2019, individuals age 70½ and older can continue contributing to their IRAs as long as they have earned income (generally, work-related earnings). However, if you make deductible contributions after age 70½, the amount of any QCD made at any point in the future will be taxable up to the value of those contributions.

Private foundations, donor-advised funds, supporting organizations (as defined by the IRS), charitable gift annuities, and charitable remainder trusts are ineligible to receive QCDs.